What Is Redeployment, and Why Is It Sometimes Necessary?

Redeployment can often be a “taboo” topic in the EB-5 industry. Many investors do not understand what it is, how it works, or why it may be needed. With recent changes and a subsequent legal challenge to USCIS sustainment period policy, the redeployment of funds has been placed firmly in the limelight.

Redeployment represents one of the biggest risks involved in an EB-5 investment. As a result, we want you to be fully informed on this subject so you can make the best investment decision for you and your family.

Any investment in which EB-5 funds may need to be redeployed raises three key concerns. First, how likely are funds to be redeployed? Second, what is the track record of the EB-5 fund manager responsible for redeploying EB-5 funds? Third, how likely is the redeployment project to succeed?

Redeployment is sometimes necessary due to a requirement that EB-5 investors’ funds remain invested for a specific period, referred to as the sustainment period. The sustainment period, also referred to as the “at-risk period,” is the time during which an EB-5 investor must keep his or her funds invested and at risk of loss. When a project is completed, EB-5 capital is returned to the investment fund. If this occurs before an EB-5 investor’s sustainment period has ended, that investor’s money needs to be redeployed to keep it at risk to fulfill the EB-5 program’s requirements.

In this article, we begin by looking at the current state of sustainment period policy and some uncertainty being caused by a new lawsuit. We then explore how regional centers take differing approaches to redeployment. Next, we offer some suggestions for how you can avoid redeployment. And finally, we share the key information you need to know if you cannot or choose not to avoid projects that are likely to face redeployment.

What Is Redeployment, and Why Is It Sometimes Necessary?

Recent Change and a Legal Challenge to Sustainment Period Policy

- The Original Sustainment Period (Two-Year Conditional Residence)

- The New Two-Year Sustainment Period

- IIUSA’s Lawsuit and Proposed Five-Year Sustainment Period

IIUSA Challenge to the New Sustainment Period Policy: Three Possible Outcomes

- Outcome #1: The Policy Reverts to the Original Sustainment Period

- Outcome #2: USCIS Adopts the IIUSA-Proposed Sustainment Period

- Outcome #3: The Current October 2023 Sustainment Period Remains in Effect

Differing Regional Center Approaches to EB-5 Redeployment

- EB5AN Takes a Responsible Approach to Redeployment

- Other Regional Centers Take a High-Risk Approach to Redeployment

How to Find Projects with a Lower Likelihood of Redeployment

How to Limit Your Exposure to Redeployment Risk

Recent Change and a Legal Challenge to Sustainment Period Policy

The Original Sustainment Period (Two-Year Conditional Residence)

The passage of the EB-5 Reform and Integrity Act (“RIA”) in March 2022 raised new questions about the definition of sustainment period. The RIA amended existing EB-5 regulations to state that EB-5 investor funds should remain invested for “not less than 2 years”. Prior to this change, the two-year sustainment period for an EB-5 investment was defined as the investor’s two-year period of conditional residency. So, under the pre-RIA definition, an EB-5 investor was not eligible to have his or her EB-5 investment repaid until after he or she had obtained a Conditional Green Card and held it for two years. This rule remains in effect for all those who made EB-5 investments prior to the passage of the RIA.

The New Two-Year Sustainment Period

In October 2023, USCIS published its interpretation of the changes made by the RIA related to the sustainment period. With this announcement, USCIS effectively changed the sustainment period to be only the two-year period following investment. Under this new policy, the sustainment period is no longer tied to the immigration process of an EB-5 investor. In other words, USCIS believes that, under the RIA, the investment date—not the date the investor’s Green Card is issued—determines when the sustainment period begins.

IIUSA’s Lawsuit and Proposed Five-Year Sustainment Period

On March 29, 2024, Invest in the USA (IIUSA), a membership-based 501(c)(6) not-for-profit industry trade association for the EB-5 Regional Center Program, filed a lawsuit against USCIS. This lawsuit was filed without notice to IIUSA members under a decision made by its board of directors. In the lawsuit, IIUSA challenges the new two-year sustainment period policy outlined above on the basis that it was implemented improperly. The lawsuit seeks to have the policy reversed, leading to sustainment period reverting to its pre-RIA definition.

Beyond this lawsuit, IIUSA has proposed a new rule to increase the required sustainment period to five years.

If successful, this lawsuit and proposal would affect the sustainment period for thousands of EB-5 investors who filed immigrant petitions after the RIA was passed in March 2022.

IIUSA’s Challenge to the New Sustainment Period Policy: Three Possible Outcomes

IIUSA’s lawsuit has created uncertainty around the EB-5 sustainment period. We see three possible outcomes to this lawsuit and IIUSA’s proposed five-year rule. Which outcome becomes reality will depend on two main factors. Also, it’s important to keep in mind that any of the three outcomes will apply retroactively to all post March 2022 EB-5 investors.

First, the outcome will depend on whether the IIUSA lawsuit succeeds or fails. Second, it will depend on whether or not USCIS moves forward with new notice-and-comment rulemaking.

Each of the three likeliest outcomes would have a different impact on EB-5 investors and EB-5 fund redeployment.

The following are what we believe to be the three most likely sustainment periods that could come about as a result of the IIUSA lawsuit:

Outcome #1. The policy reverts to the original sustainment period that coincides with the two-year period of conditional residency. This would be the case if IIUSA’s lawsuit succeeds.

Outcome #2. IIUSA’s proposed five-year sustainment period policy is adopted. This would be the case if the lawsuit succeeds and USCIS proposes the five-year policy as a new rule through proper notice-and-comment rulemaking.

Outcome #3. The October 2023 policy remains in effect, which means a fixed two-year sustainment period. This would be the case if IIUSA’s lawsuit fails. Alternatively, this could also happen if the lawsuit succeeds but USCIS proposes the two-year policy through normal notice-and-comment rulemaking.

Whether or not investors’ EB-5 funds will need to be redeployed into one or more investments after the original investment is repaid will largely depend on the outcome of this lawsuit and any subsequent rulemaking. But EB-5 investors will also be impacted in different ways depending on their individual circumstances.

A given investor’s need for EB-5 fund redeployment is affected by his or her country of birth. Known as a person’s country of chargeability, where an investor is from makes a difference because some countries are subject to visa retrogression. A limited number of visas are available under each visa category each year, and these are further divided by country. When the number of applicants from a given country exceeds the number of available visas for that year, applicants must wait for a future round of visas to become available. In the case of backlogged EB-5 applications from high-demand countries like China and India, this wait can take several years.

Another factor affecting the need for redeployment is project type and duration. For instance, new data suggests that the urban TEA visa set-aside category is likely already oversubscribed, particularly for Indian and Chinese investors. As a result, EB-5 investors in urban TEA projects are more likely to face retrogression. And, in general, projects with shorter investment durations are more likely to result in one or more redeployments.

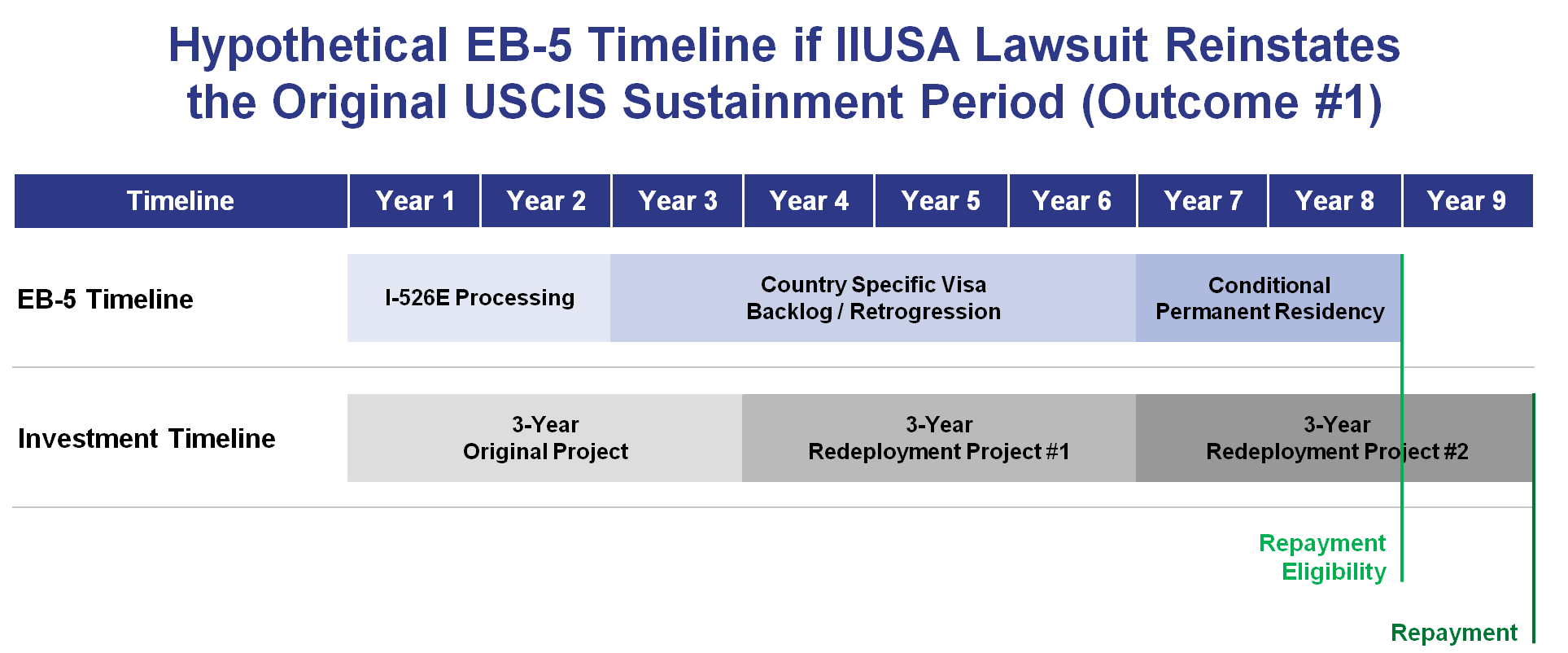

Outcome #1: The Policy Reverts to the Original Sustainment Period

One possible outcome is that the IIUSA lawsuit succeeds. If Outcome #1 happens, the sustainment period would revert to the original requirement in place prior to October 2023.

In this case, the funds of many investors would be at higher risk of needing to be redeployed. Since October 2023, many investors have invested in short-term projects, such as urban TEA projects with two- to three-year terms. After the original two- to three-year investment is completed, many investors will not have even begun their two-year conditional residency period. This is particularly true for Chinese and Indian investors. Under the original sustainment period policy, these investors’ funds would have to be redeployed to remain at risk.

As an example, consider an Indian investor who selected a three-year urban TEA project. Because of a high volume of urban TEA investors already in line, visa retrogression may cause this investor to wait up to six years to receive a temporary Green Card. Under the original sustainment period policy, the investor would have to hold this Green Card for two full years before becoming eligible for repayment. If the investor does not receive a temporary Green Card until year six, and that Green Card must be held for two years, then the total investment period would be eight years. Since this investor’s initial investment lasts only three years, the funds would need to be redeployed for at least another five years to remain at risk through the full sustainment period.

In this example, for the investor to immigrate and be repaid, the first investment must succeed. It must create all the required jobs and return 100% of the principal investment. Then, a second investment must also succeed and return 100% of the principal investment. If the second investment does not last for at least five years, a third investment would be needed. For such an investor, the advertised three-year term would become much longer. Instead of a single investment, the EB-5 investor’s funds would be used for multiple investments.

The following is an illustration of a potential timeline for an EB-5 investor under this outcome.

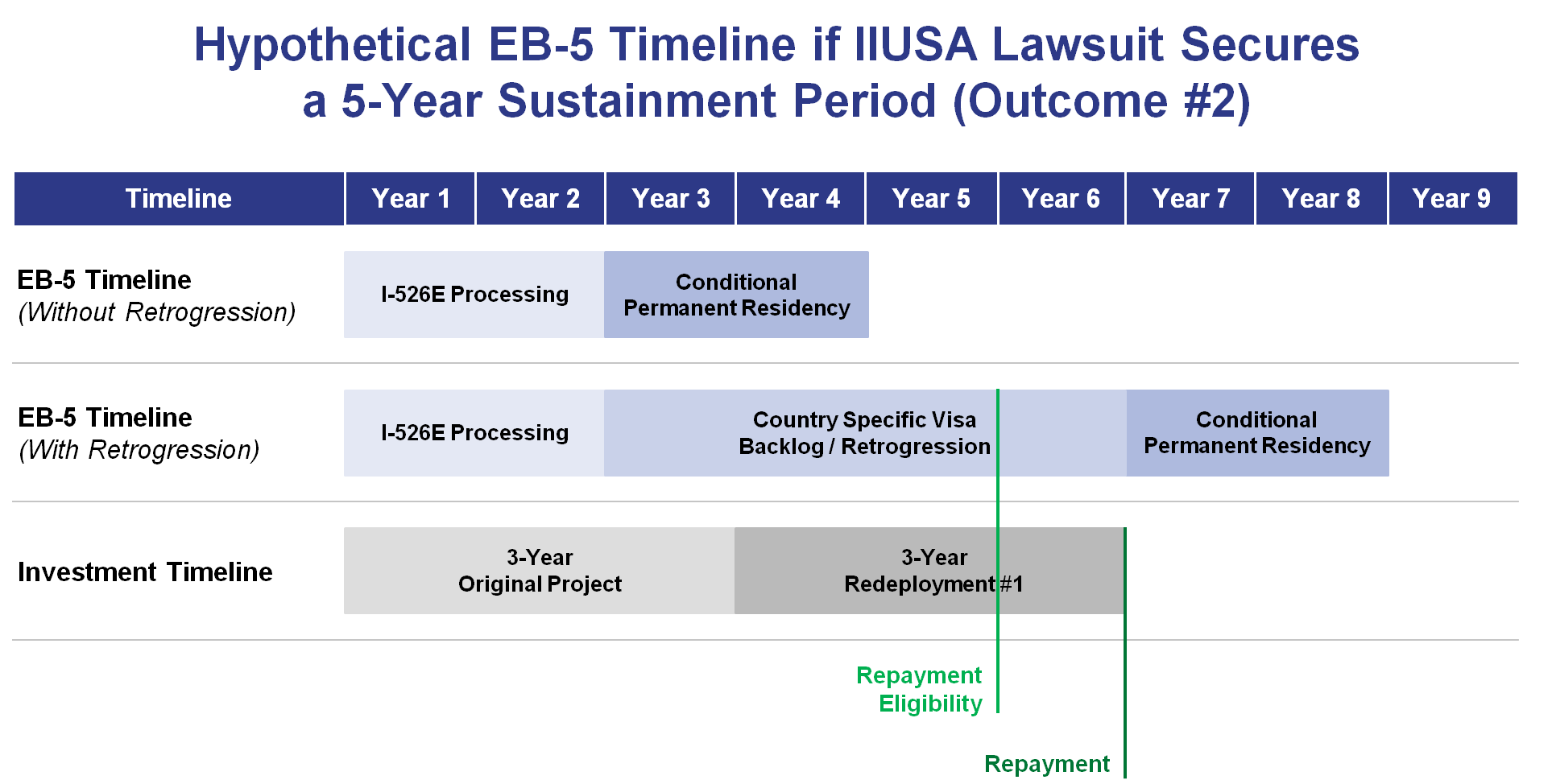

Outcome #2: USCIS Adopts the IIUSA-Proposed Sustainment Period

If the IIUSA lawsuit succeeds, USCIS may move forward with new notice-and-comment rulemaking. If USCIS were to adopt the five-year sustainment period policy proposed by IIUSA, a similar outcome to outcome #1 would occur.

In the case of Outcome #2, EB-5 funds would need to be deployed for a total of five years from the date of investment. The IIUSA proposal is similar to the current October 2023 policy in that the length of the investment is fixed. But the length of time the EB-5 funds must remain at risk would be closer to the original sustainment period.

Note that for investors facing retrogression, this would be a slightly more positive outcome than Outcome #1. However, for investors who are not subject to visa retrogression, Outcome #2 would require them to keep their funds at risk longer than under the current policy. For most investors who are not subject to retrogression, Outcome #2 would likely result in the longest sustainment period.

Under this outcome, for any investments with terms of less than five years, EB-5 funds will need to be redeployed, with only one redeployment likely to be needed.

The following is an illustration of a potential timeline for an EB-5 investor under this outcome.

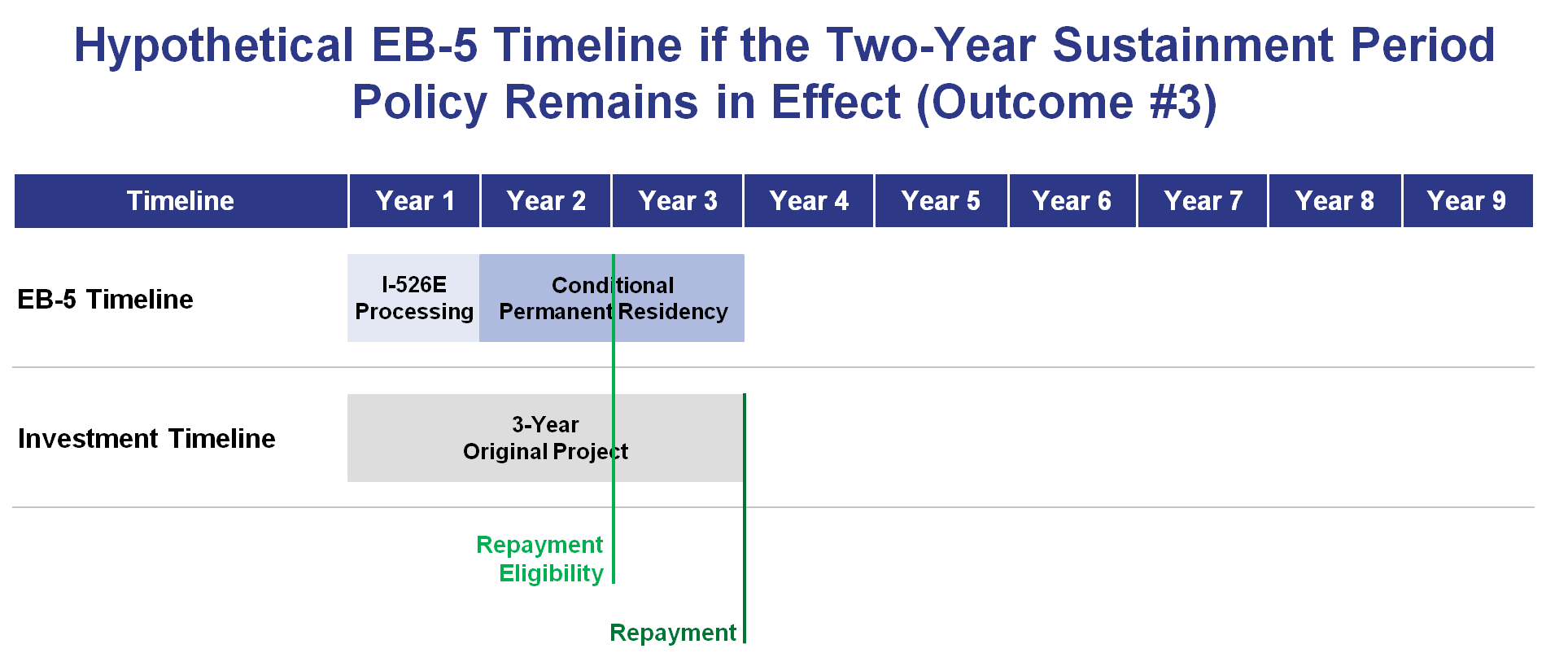

Outcome #3: The Current October 2023 Sustainment Period Remains in Effect

Of the three likely outcomes of the IIUSA lawsuit, Outcome #3 is the most favorable to EB-5 investors. This outcome could occur if the IIUSA lawsuit fails or if the lawsuit succeeds but USCIS puts the policy in place through proper rulemaking.

The sustainment period for Outcome #3 is fixed at two years. This means it would not be impacted by current or future visa retrogression. With the shortest sustainment period of the three likely outcomes, Outcome #3 offers the lowest probability of redeployment.

The following is an illustration of a potential timeline for an EB-5 investor under this outcome.

Differing Regional Center Approaches to EB-5 Redeployment

How an EB-5 regional center approaches redeployment can have a major impact on a project’s EB-5 investors. If a regional center does not follow USCIS policy and keep its funds at risk, its EB-5 investors will likely fail to obtain their permanent Green Cards. This means regional centers frequently need to redeploy EB-5 funds.

During redeployment, regional centers often have significant power to decide where EB-5 funds are redeployed. Indeed, investors sometimes have limited say over such decisions. While some regional centers choose a measured approach to redeployment, this is not always the case. In the past, many regional centers have taken advantage of EB-5 investors by redeploying EB-5 funds into high-risk, long-term investments for their own gain.

Below, we will discuss two major approaches to redeployment: the responsible approach that some regional centers take, and the irresponsible approach taken by others.

EB5AN Takes a Responsible Approach to Redeployment

Over the years, many of our EB-5 investors born in China and India have been negatively affected by visa retrogression. Several of our investments were 100% successful, created all the required jobs, and returned funds on time—or even early. In short, these projects went according to plan. Even so, for our EB-5 investors who had not yet completed the required sustainment period and wished to continue with the EB-5 immigration process, funds had to be redeployed. As discussed above, redeployment was necessary to keep these investors eligible for their permanent U.S. Green Cards.

When EB5AN has had to redeploy funds for investors, we have redeployed investor capital into similar real estate development opportunities. We found investments in the same general geographic area with the same risk profile, the same project developer, and the same investor return as the original EB-5 investment.

For example, EB5AN’s Saltaire St. Petersburg waterfront condominium project by Kolter was completed in Q4 of 2023. The project was a success, creating over 2,000 EB-5 jobs. Kolter repaid 100% of the EB-5 equity investment principal. Since the project’s EB-5 investors weren’t eligible for repayment, EB5AN redeployed EB-5 funds into a similar waterfront condominium project by Kolter in Sarasota, Florida.

EB5AN takes additional steps to ensure investors are fully informed and their redeployed funds are being used in compliance with USCIS policy. For instance, EB5AN has engaged Klasko Immigration Law Partners, a leading EB-5 law firm, to advise EB5AN on redeployment situations. Klasko also provides information for investors about the required sustainment period and context for why redeployment may be necessary.

Other Regional Centers May Take an Irresponsible, Higher-Risk Approach to Redeployment

As mentioned earlier, many other regional centers approach redeployment in a manner that may not serve the best interests of their EB-5 investors. Often, other regional centers view redeployment as an enormous source of potential profit. In these cases, the aim is to make the most money possible. They maintain this approach even if that means redeploying funds into investments with comparably higher risk than the original investment that investors signed up for.

With redeployment, regional centers are not putting their own funds at risk. Since they do not face any meaningful risk themselves, they are incentivized to “swing for the fences,” so to speak. They may go for a “home run” investment in hopes that they can realize significant profits. In such cases, these regional centers have essentially no downside. None of their own money is at risk—instead, the EB-5 investors take on all of this risk.

With the required sustainment period now in question, it is critical for investors to read through a potential EB-5 project’s offering documents and understand the process and the key terms that would govern any required future redeployment of funds.

How to Find Projects with a Lower Likelihood of Redeployment

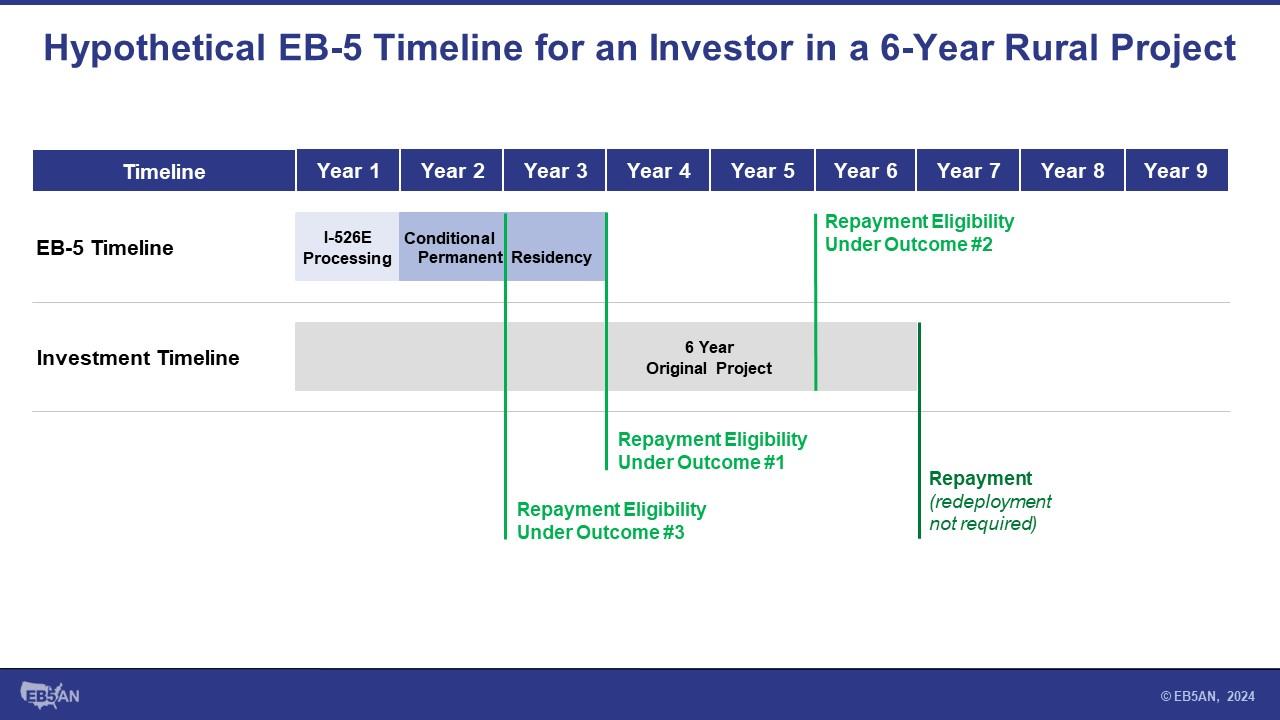

By selecting the right project, EB-5 investors may avoid redeployment entirely. Two project features help EB-5 investors avoid redeployment. These two features are rural TEA designation and longer investment terms.

Rural TEA projects provide faster I-526E processing. This means investors receive their temporary Green Cards more quickly, which helps ensure that the two-year period of conditional residency begins as soon as possible. If Outcome #1 becomes reality, priority processing will be especially helpful.

Rural TEA projects also have a larger pool of set-aside EB-5 visas. With more visas set aside, EB-5 investors in rural TEA projects are less likely to face visa retrogression. As a result, they are less likely to need their funds redeployed.

Longer investment terms are typically found in projects structured as loans. A longer-term loan is one that does not mature for five years or more. With longer loan terms, investors are more likely to have met their sustainment periods by the time the loan is repaid. This is true regardless of which of the three outcomes becomes reality. In other words, since EB-5 funds would be at risk for at least five years, investors would likely have already completed their period of conditional residency by the time the loan matures, satisfying the sustainment period under Outcome #1. Loans of five years or more also easily meet the sustainment periods under Outcome #2 (five years) and Outcome #3 (two years).

The following is an illustration of a potential timeline for an EB-5 investor who chooses to invest in a longer-term rural TEA deal. The illustration shows how such a deal is likely to meet the sustainment period in any of the outcomes discussed above.

One downside to this approach, of course, is that funds will be invested for at least five years. Therefore, if IIUSA loses its lawsuit or USCIS engages in proper rulemaking to bring about Outcome #3, funds will be invested for a few years longer than necessary. But a longer-term investment that accounts for all three potential outcomes is at less risk of needing to be redeployed.

Ultimately, this entire discussion hinges on risk and reward. Redeployment is a risk for investors with no corresponding reward. The best scenario for EB-5 investors in terms of risk is to have their funds invested only once.

EB5AN has always believed that the right way to approach redeployment is to minimize the risk to EB-5 investors. In light of the current uncertainty surrounding the sustainment period policy, we believe the best choice is to structure deals that account for any of the three likeliest outcomes. Because of this, we tend to favor investments with ample investment periods.

Some investors evaluate redeployment risk differently than we do. This is understandable. Our goal is to make choices that generally protect our investors and to ensure that investors have as much relevant information available to them as necessary to make fully informed decisions.

How to Limit Your Exposure to Redeployment Risk

If you decide to select a non-rural TEA project or a project with a very short investment timeline, the chances of having your funds redeployed are materially higher. But even if you choose a rural TEA project with a five-year loan term, you may still face redeployment. In any event, EB-5 investors can take steps to limit their risk if their funds have to be redeployed.

One of the best resources you have for avoiding risk is also one of the simplest: You can ask questions about an EB-5 regional center’s redeployment track record. We suggest both asking these questions and receiving their answers in writing. Asking some key questions will help you assess how much risk you may face if your funds are redeployed. If the regional center has never redeployed funds, it will be difficult to gauge what approach it may take.

Here are some of the best questions to ask to assess a project’s risk surrounding redeployment:

- For which projects has the regional center redeployed EB-5 funds in the past?

- Were investors who opted not to continue their immigration process allowed to exit before redeployment?

- How did the risk profile and investment term of each redeployment investment differ from the original investment?

- Was each redeployment investment in the same geographic area and the same industry as the original investment?

- Was the developer for each redeployment investment the same as the original project?

- Did each redeployment investment have the same anticipated total return on investment?

Redeployment is complicated, and all EB-5 projects are different. To avoid unnecessary risk, you need to understand all aspects of your investment. This includes the possibility that your funds may need to be redeployed. Book a call today with our team to discuss any questions you may have related to redeployment, rural TEA projects, or anything else related to EB-5.