The EB-5 Investor Visa offers a path to U.S. residency for African investors, contingent upon stringent Source of Funds (SoF) documentation. The recent webinar led by Simone Williams, managing partner of Williams Global Law, PLLC, provided a wealth of information tailored to address the unique hurdles African investors face in complying with USCIS SoF requirements.

Watch the Full Webinar: EB-5 Source of Funds for African Investors

What Is Source of Funds? How Does It Fit with EB-5?

Eligible Sources of Funds

Source of Funds Case Study: Loan Secured by Real Estate

EB-5 Visa Issuance Analysis for African Countries

Unique Situations for Investors from African Countries

Next Steps for African EB-5 Investors

What Is Source of Funds? How Does It Fit with EB-5?

Source of Funds is the documentation of an EB-5 investor’s lawful source of investment capital. The U.S. government must be satisfied the funds have been lawfully obtained.

Per USCIS requirements, an EB-5 investor must invest his or her own capital, establish that they are the legal owner of the capital invested, and they obtained the capital through lawful means, in addition to documenting the path of the funds to establish that the investment was made or is actively in the process of being made.

The two required components of an I-526E petition are:

- Project documentation explaining how the investment satisfies EB-5 criteria.

- SoF evidence showing that the investment capital is eligible.

USCIS must approve both components for an investor’s I-526E to be approved.

Eligible Sources of Funds

Ordinary Income

Ordinary income is money earned by the investor or spouse such as salary, sole proprietorship income, stock dividends, and business dividend distributions.

- Ordinary Income: Best Practices

Identify whether income is earned through self-employment or third-party employment. The documentation changes significantly based on who the investor’s employer is.

Third-party employment: Include paystubs, employment contract and confirmation letter, and bank statements showing accumulation and maintenance of funds.

Self-employment: Show the source of funds utilized to start the business. Include documents such as invoices/purchase orders, business bank statements, and personal bank statements.

- Ordinary Income: Common Problems

Translation of foreign documents: Include certified translation of all non-English documents including employment records, salary certificate or proof of dividend distribution, bank statements, and tax returns.

Proving appropriate taxes have been paid: Include tax returns showing income from all sources. Show proof that taxes have been paid (withheld), and the amount of after-tax funds matches the amount of funds remaining in the respective accounts.

Tracing from source to current account: Include bank records showing after-tax funds first entering the EB-5 investor’s account and then moving from account to account until the funding of the EB-5 investment (ideally without commingling with other funds).

Capital Gains

Capital gains are money earned by the investor or spouse from the sale of an asset for a gain on investment such as real estate, business, and securities.

- Capital Gains: Best Practices

Focus on the initial principal investment made in assets such as real property, equity, or fixed deposits.

Real property: Properly document the income used to fund the purchase price of the property. If capital gains were received from real estate flipping, provide purchase and sale deeds and corresponding bank statements of all properties leading up to the property sold to fund the EB-5 investment.

Sale of company: Trace back funds to the initial investment in the investor’s company. The investor must prove source of funds from the inception of the company together with tax returns and financial statements of the company for the last seven years. Document proper registration and lawful activity of the company. Investor must provide sales agreement and corresponding bank statements reflecting receipt of sales proceeds.

- Capital Gains: Common Problems

Translation of foreign documents: Include certified translation of non-English documents including sale agreement(s), asset valuation, bank statements, and tax returns.

Proving appropriate taxes have been paid: Provide tax returns showing income from all sources. Show proof that taxes have been paid (withheld), and the amount of after-tax funds matches the amount of funds remaining in the respective accounts.

Tracing from source to current account: Include bank records showing after-tax funds from the sale first entering the EB-5 investor’s account and then moving from account to account until the funding of the EB-5 investment (ideally without commingling).

Gifts or Inheritance from Family or Friends

Gifts are money gifted outright, with no expectation of repayment to the investor or spouse. Inheritance is funds willed to the investor or spouse.

- Gifts or Inheritance from Family or Friends: Best Practices

Establish that the investor is the rightful heir of the asset(s) and document how the initial asset was purchased by the donor.

Evidence of inheritance: Always provide a will and testament when available. If no will exists, provide local rules of intestate succession.

Source of funds: Include evidence of how the inherited property was acquired by the donor. The evidence can be in the form of sworn affidavits from donor and/or third parties with knowledge, but documents proving source of funds of donor are the safest.

- Gifts or Inheritance from Family or Friends: Common Problems

Proving appropriate taxes have been paid:Include certified translation of foreign documents such as gift agreement, personal documents of the donor, bank statements, and tax returns.

Tax returns showing income from all sources: Include proof that gift and probate taxes have been paid, and the amount of after-tax funds matches the amount of funds remaining in the respective accounts.

Tracing from source to current account: Provide bank records showing after-tax funds from the gift or inheritance first entering the EB-5 investor’s account and then moving from account to account until the funding of the investment (ideally without commingling).

Loans from Third Parties

A loan from third parties is money lent to the investor or spouse at market terms from a third party against sufficient asset(s) owned by the investor or spouse.

- Loans from Third Parties: Best Practices

A personal loan must have terms comparable to a commercial bank loan. In the case of a loan from a person or non-financial institution, the lender must provide documentation of source of funds.

Source of funds of the collateral asset: Provide evidence of how the investor acquired the asset used as collateral. The ideal option is to acquire an uncollateralized loan from a financial institution because it avoids problems of proving source of collateral.

Source of funds of lender: When borrowing from a company, provide evidence of establishment and lawful operations of the company, evidence of the investor’s ownership of the company if applicable, the value of the investor’s ownership, and the financial status of the company with tax returns and financial statements.

Documents: Submit evidence of ownership of collateral, valuation report of the collateral asset, and proof of the ability of the lender to foreclose in case of non-payment of loan.

- Loans from Third Parties: Common Problems

Translation of foreign documents: Provide certified translation of non-English documents including the loan agreement, note, personal guaranty, mortgage lien, bank statements, and tax returns.

Proving appropriate taxes have been paid: Include tax returns showing income from all sources, and proof that all relevant taxes were paid.

Tracing from source to current account: Provide bank records showing how the lender obtained the funds (legally earned and taxes paid on them) and how the investor used the funds since obtaining them from the lender before the EB-5 investment (ideally without commingling).

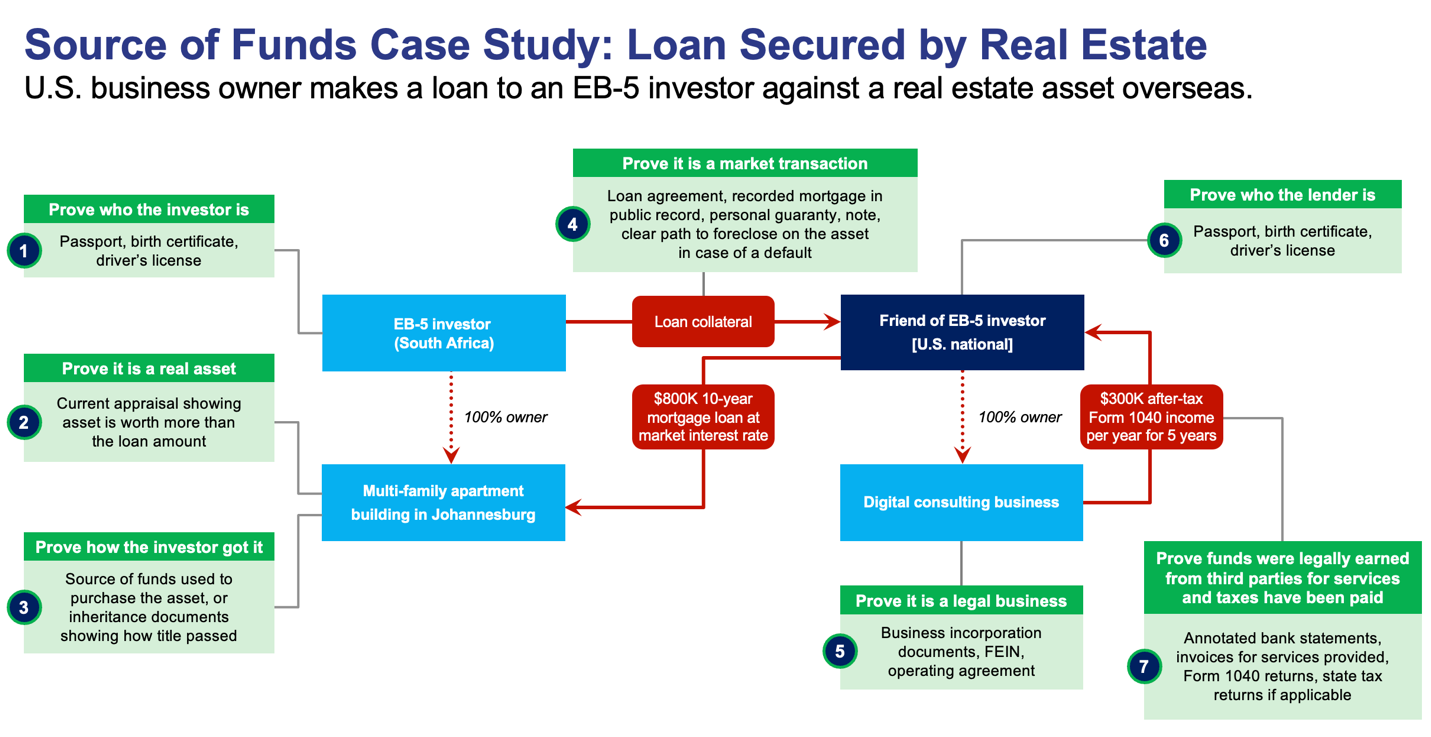

Source of Funds Case Study: Loan Secured by Real Estate

A business owner in the United States makes a loan to a South African EB-5 investor against a real estate asset overseas in Johannesburg.

Read this post for more details on proving source of funds derived from a loan-based asset.

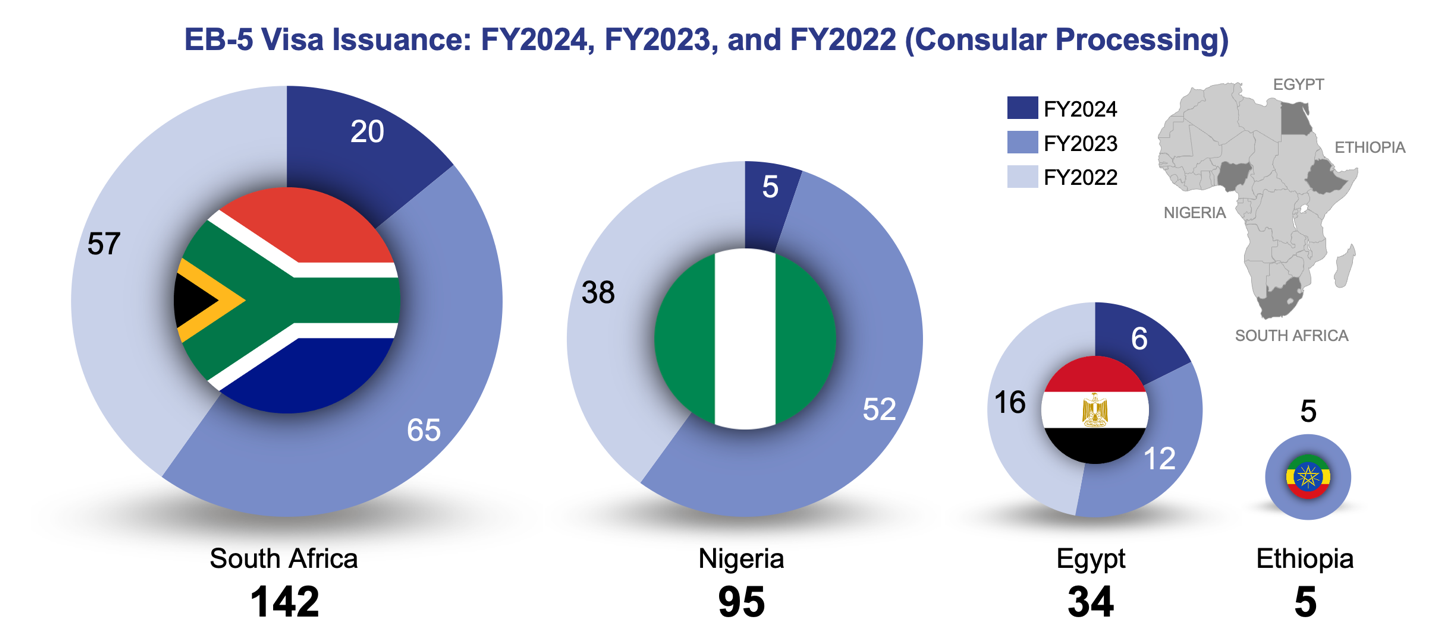

EB-5 Visa Issuance Analysis for African Countries

According to the number of EB-5 visas issued through consular processing over the previous three years, South Africa leads all other African countries in EB-5 visa issuance, followed by Nigeria and Egypt.

Source: IIUSA EB-5 Visa Data Dashboard

Unique Situations for Investors from African Countries

South Africa

South Africa has strict foreign exchange controls and therefore investors may only transfer a maximum of R10 million (approx. USD 532,000) for foreign investment allowance. To successfully transfer funds in compliance with local rules and regulations, investors should work closely with an experienced EB-5 immigration attorney who has worked with other South Africa-based investors.

Nigeria

Due to Nigerian restrictions on citizens purchasing USD in the official market and the scarcity of foreign exchange, particularly US dollars, Nigerian citizens may be required to purchase USD from the parallel market with third-party providers for personal investment and business needs.

French-speaking African countries (e.g., Benin, Togo, Cameroon)

French-speaking West African countries have strict foreign exchange requirements and need permission from the government to transfer foreign currency. Transactions requiring foreign exchange must be duly documented and approved by the exchange control authorization.

Ethiopia

There is a limitation on acquiring USD in Ethiopia, along with an inability to transfer BIRR out of Ethiopia. Ethiopian EB-5 applicants are advised to seek specialized counsel on how they can transfer and/or acquire USD to contribute to the EB-5 project.

Next Steps for African EB-5 Investors

The EB-5 source of funds requirement, while complex, is navigable with meticulous planning and expert legal support. Investors are encouraged to employ a proactive approach, maintaining records and seeking advice early in the process.

For additional resources and personalized consultation, investors can reach out to Simone Williams at simone@williamsgloballaw.com or +1 (202) 753-5075.

For further guidance on how to navigate the EB-5 program and how to select a safe project, we invite you to schedule a free consultation with EB5AN.

Disclaimer: This article is not legal advice and is for informational purposes only. Investors are urged to engage their own legal counsel for individual legal advice.