Under the second Trump administration, and particularly in 2026, USCIS has taken a stricter approach toward adjudicating EB-5 filings. Investors are seeing more RFEs, NOIDs, and denials at both the I-526E and I-829 stages. These unfavorable decisions from USCIS are not limited to larger issues such as incomplete filings or failed projects. USCIS is now questioning source-of-funds records, loan structures, partial funding, job creation, sustainment, redeployment, and even prior immigration history.

This shift in adjudication trends comes at an important time for EB-5 investors. Current grandfathering protections provide that regional center investors who file by September 30, 2026, receive protection against a lapse in Regional Center Program authorization. EB-5 investment amounts are expected to increase in 2027, and the Regional Center Program is up for renewal in September 2027.

For investors preparing to file, and for families that already hold conditional Green Cards, consulting with a skilled immigration attorney has become more important than ever.

To address these trends, EB5AN held a webinar hosted by managing partners Sam Silverman and Mike Schoenfeld, as well as senior VP Ahmed Khan. The discussion featured Ron Klasko, chairman of Klasko Immigration Law Partners. Klasko is one of the most experienced EB-5 immigration attorneys in the industry and a leading voice on EB-5 litigation, source-of-funds issues, and I-829 denials.

We give Klasko Immigration our highest recommendation for all matters related to EB-5 and immigration law generally.

This article summarizes the key points discussed and explains what EB-5 investors should know now. It covers the main denial risks at the I-526E stage, the good-faith investor protections created by the RIA, the growing risks at the I-829 stage, and the practical steps investors can take to reduce immigration risk before USCIS raises questions.

Highlights: I-526E Denial Trends:

Highlights: I-829 Denial Trends:

Full Webinar:

I-526E Denial Risks: Source of Funds, Loans, Partial Funding, and Investor Records

- Regional Center-Linked Loans Are Receiving Closer Review

- Partial Funding Can Create Serious Filing Risks

- USCIS Is Looking Beyond the Basic Source-of-Funds Story

- Prior Immigration Records Can Affect the I-526E Filing

- Real Estate Proceeds Can Lead to Older Documentation Requests

Good-Faith Investor Relief: Regional Center Termination, Debarment, and Reinvestment Options

- Regional Center Termination

- Debarment Remains Unclear

- Reinvestment May Help Some Investors Preserve Their EB-5 Cases

I-829 Denial Risks: Job Creation, Sustainment, Redeployment, and Immigration Court

- Job Creation Is the Central I-829 Issue

- Sustainment Is Becoming a More Complicated Issue

- Redeployment Is Receiving New Attention

- Faster I-526E Adjudications Can Create Timing Problems

- USCIS Is Reexamining Source of Funds at the I-829 Stage

- Immigration Court Creates Delay and Uncertainty

- What Happens After an I-829 Denial

EB-5 Investors Should Prepare Before USCIS Raises Questions

I-526E Denial Risks: Source of Funds, Loans, Partial Funding, and Investor Records

The I-526E petition focuses on two main issues. The first is the EB-5 project. The second is the investor’s source of funds.

For many investors, the project side is easier to evaluate when the regional center has already obtained Form I-956F approval. That approval means USCIS has reviewed the project-level materials and determined that the project meets EB-5 requirements. But I-956F approval does not remove the investor’s burden. The investor still has to prove that the EB-5 capital came from a lawful and traceable source of funds

That is where many I-526E issues now begin. USCIS is taking a closer look at source-of-funds records, loan arrangements, partial-funding structures, and prior immigration filings. A case that may have been approved one or two years ago may now receive an RFE, NOID, or denial if the documentation leaves room for questions.

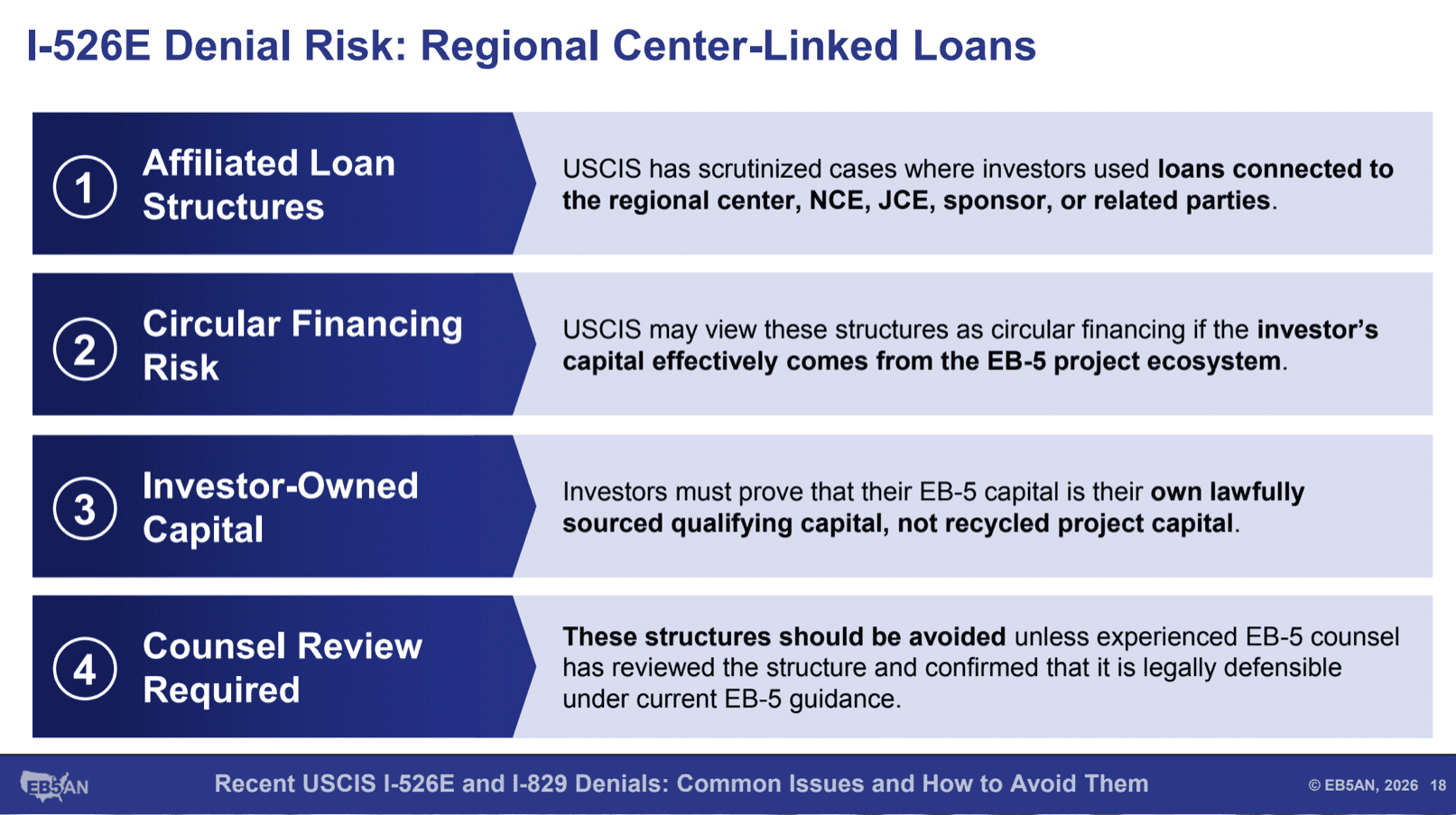

Regional Center-Linked Loans Are Receiving Closer Review

One of the most closely watched issues is the use of regional center-linked loans. These are loans arranged through or connected to a regional center and used by the investor as part of the EB-5 investment funds.

Such loans may be lawful if structured correctly. The problem is that they can raise both legal and appearance-based concerns. USCIS may question whether the loan is a real financing arrangement or whether it is simply a circular transaction. In the worst case, the arrangement can look as if the regional center is lending money to the investor, and the investor is immediately sending the same money back to the regional center.

The RIA added two requirements: Any loan used in an EB-5 filing must be bona fide, and it also cannot be used to avoid the minimum investment amount.

A stronger loan structure should show that the loan is real. The loan should include commercially reasonable interest, repayment terms, and default provisions. Collateral can also help. It is also better when the loan is subject to genuine underwriting, so that some investors may be approved and others may not. If every investor automatically receives the loan, USCIS may look more closely at the arrangement.

The identity of the lender also matters. A bank lender is usually cleaner from a source-of-funds standpoint. A non-bank lender can create more questions because USCIS may ask for the lender’s own source of funds. That can lead to a commingling issue and force the investor to document money that did not originate with the investor.

If the loan has already been repaid, or if the investor can show the ability to repay it, that may help prove that the loan is bona fide. But investors should not assume that a loan structure will be accepted simply because similar cases were approved in the past. USCIS policy and adjudication trends can change. A structure that once moved through USCIS without much resistance may now face a much deeper review.

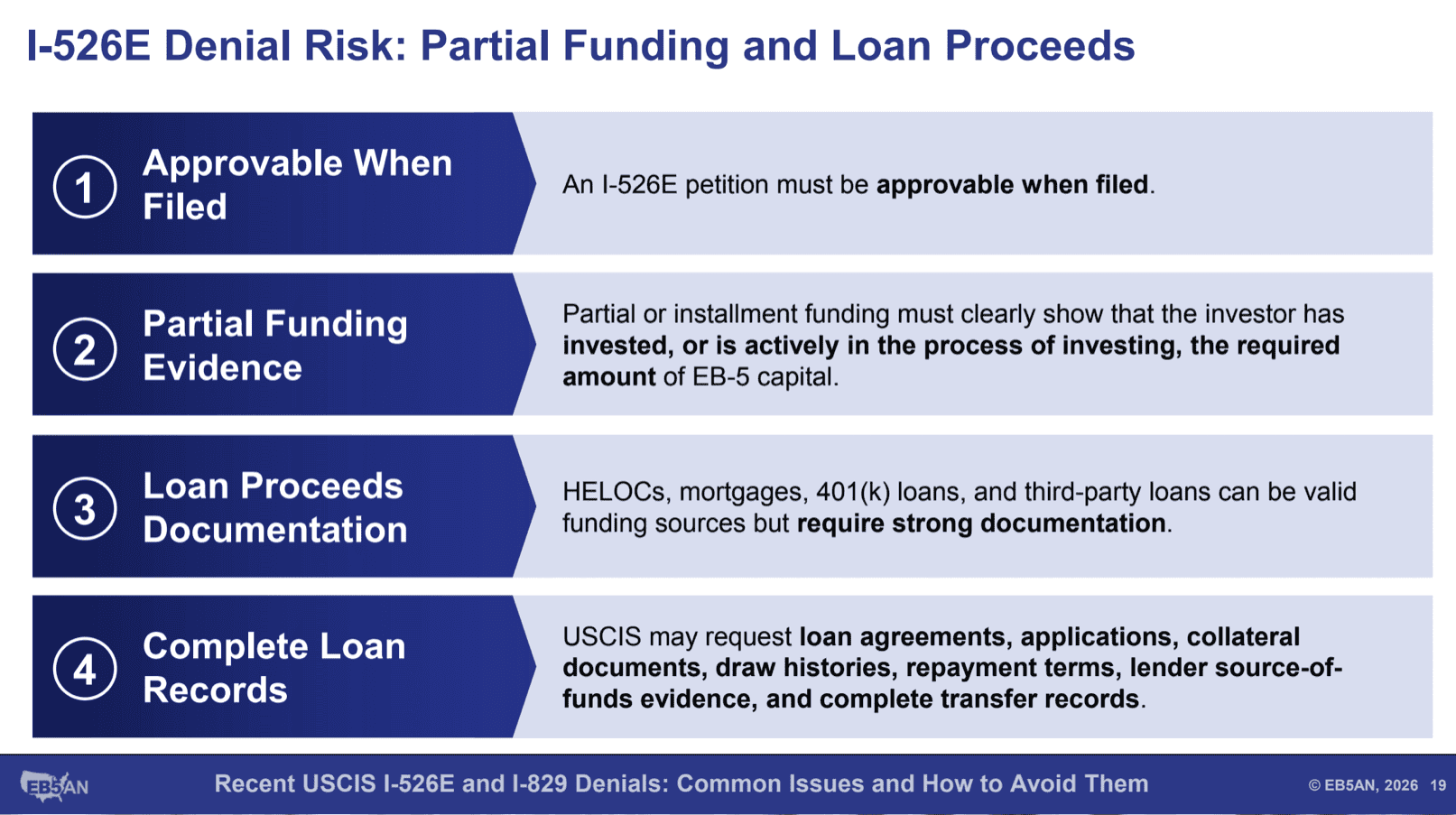

Partial Funding Can Create Serious Filing Risks

Partial funding is another major I-526E issue. Many investors use partial funding to invest the required $800,000 in installments rather than all at once. In some cases, investors do this because of currency-export restrictions in their home country. In other cases, they want to file before a deadline while they are still arranging the rest of their capital.

USCIS has approved partial-funding cases in the past. But these cases are now getting closer scrutiny. USCIS may hold investors to the original equity commitment and may resist later extensions, substitutions, or changes to the funding plan.

A partial-funding case needs to be carefully documented from the beginning. The investor should have an irrevocable written commitment to complete the full investment. The filing should include a definite date by which the remaining funds will be invested. The investor should also document the lawful source of funds for the full $800,000 at the time the I-526E is filed.

It is not enough to show the source of funds for only the first installment. If an investor files with $500,000 and plans to contribute the rest later, the investor should already be able to show where the remaining $300,000 will come from. The case should not depend on uncertain future events, such as a possible bonus, a possible family loan, or assets that may or may not become available later.

Several risks can arise after filing. USCIS may decide that a petition was not approvable when filed because the investor had not yet invested the full $800,000. USCIS may also adjudicate the petition before the investor has completed the funding. That can create a denial risk even if the investor always intended to finish the investment.

A separate risk arises if the investor documents one source of funds at filing but later completes the investment with a different source. USCIS may treat that as a material change. For that reason, the funding plan at filing should match the way the investment will actually be completed.

Some investors choose to interfile proof after they complete the full investment. That may help avoid a denial based on incomplete funding. But interfiling has its own problems. The evidence must actually reach the file, and there can be practical uncertainty about whether USCIS will review it before making a decision.

When possible, the safer route is to make the full investment up front. If partial funding is necessary, the investor should get legal advice before filing and should make sure the record is strong enough to withstand current USCIS scrutiny.

USCIS Is Looking Beyond the Basic Source-of-Funds Story

Many investors assume their source of funds is simple. A salary, RSUs, a property sale, or savings may appear straightforward. But USCIS is now looking beyond the headline explanation.

The investor still has the burden to prove that the funds were lawfully obtained. USCIS may ask for more tax records, more bank statements, more evidence of asset ownership, and more explanation of small deposits or transfers that appear in the record.

One recurring issue is tax returns. USCIS may argue that the investor submitted only five years of tax returns when the regulations refer to seven years, where applicable. This can happen even when the five years submitted show enough income to explain the EB-5 funds. The legal point may be debatable, especially where older tax returns are not applicable. But as a practical matter, investors should expect USCIS to look for gaps and ask why certain records were not provided.

Bank records can create another problem. USCIS is using the term “commingling” more often. What does this mean?

If an investor shows millions of dollars of lawful employment income in a bank account, USCIS may still focus on a small unexplained deposit. Even a minor entry can become an issue if USCIS argues that unexplained funds were mixed with lawful funds in the same account.

Prior Immigration Records Can Affect the I-526E Filing

USCIS is also looking more closely at investors’ broader immigration history. Source of funds remains a central issue, but it is no longer the only area that can create problems.

Investors who file Form I-485 for adjustment of status from within the United States should expect USCIS to review their immigration record. Prior visa applications, old statements, employment history, addresses, and other immigration filings may be compared against the EB-5 record.

This review can reach far back. Investors should assume USCIS may have access to statements made in earlier applications, even a tourist visa application from more than 20 years ago. Any inconsistency in prior immigration history can create questions.

Real Estate Proceeds Can Lead to Older Documentation Requests

Real estate sale proceeds are a common source of EB-5 funds. But USCIS may not stop at the sale itself.

If an investor sells real estate for $3 million and uses that money for EB-5, USCIS may ask how the investor originally bought the property. If the property was purchased 17 years ago, USCIS may request documentation from that time. In some cases, USCIS may ask for records going back 20 years or more.

However, many investors no longer have old bank statements, loan records, or closing documents from decades earlier. Financial institutions may no longer retain them. The investor may still have a lawful source of funds, but the paper trail may be incomplete because of the passage of time.

Some of these disputes have reached federal court. In one case, the court recognized an immediate source-of-fund standard. Under that reasoning, if the immediate source of funds is the sale of real estate, the investor should not necessarily have to prove how the property was purchased 25 years earlier.

USCIS has not fully accepted that approach. More cases on this issue are still being litigated. For now, investors using real estate proceeds should be ready for USCIS to ask for the history behind the property, not just proof of the final sale.

Good-Faith Investor Relief: Regional Center Termination, Debarment, and Reinvestment Options

The RIA created protections for EB-5 investors who are harmed, through no fault of their own, by their regional center or EB-5 project. These are often called good-faith investor protections.

Before the RIA, investors had far fewer options if a regional center was terminated or a project failed. An investor could have made the required investment, acted in good faith, and still lost the immigration benefit because of problems caused by the regional center or project. Congress tried to address that unfair result by giving certain investors a way to preserve their immigration path.

The two main issues are regional center termination and project debarment. Both can affect investors who did not cause the problem but still need a way to keep their EB-5 case alive.

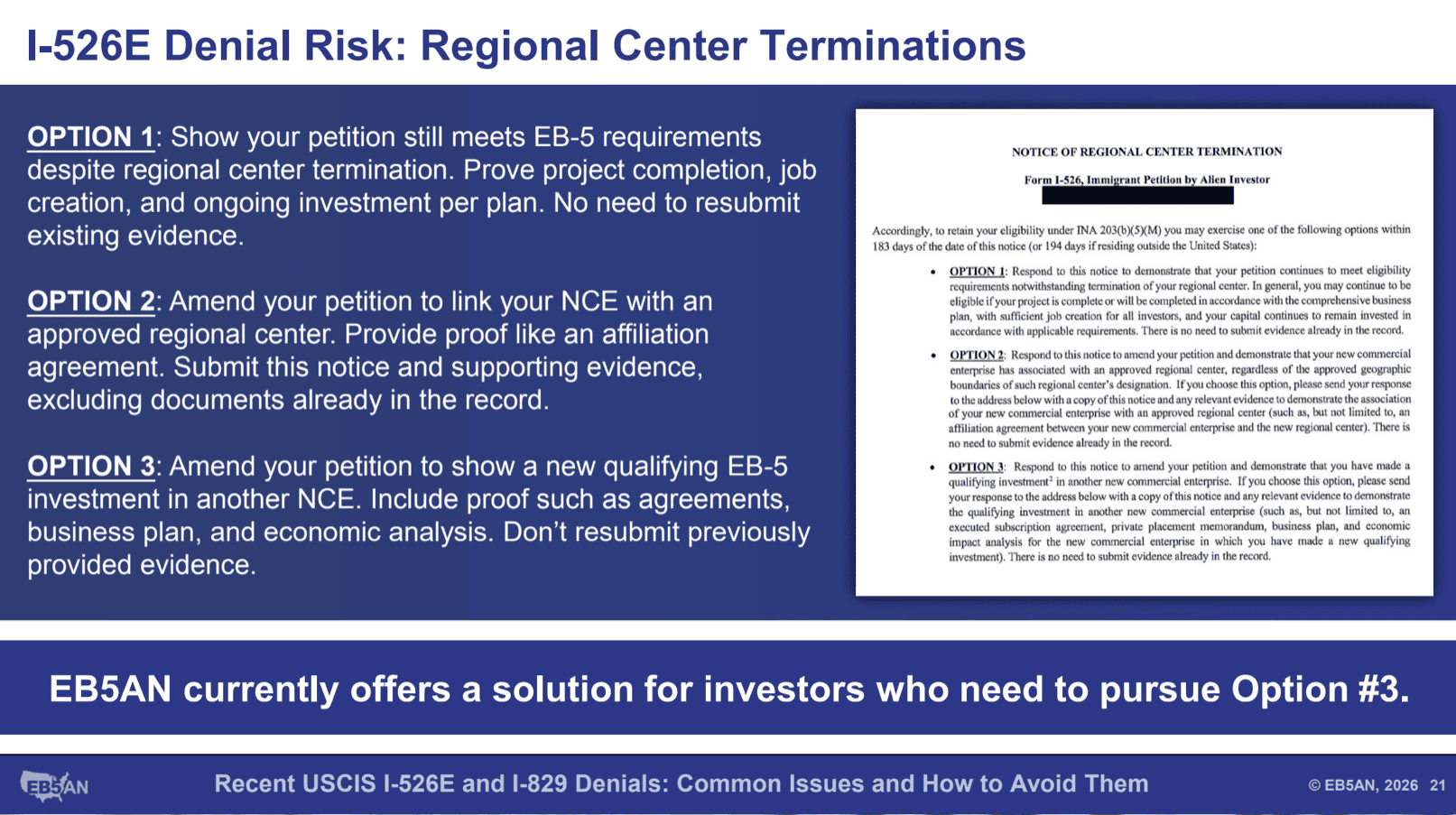

Regional Center Termination

If a regional center is terminated, the result depends on the facts. In some cases, the project itself may still be fine. If the only problem is the regional center termination, and the project has otherwise met EB-5 requirements, the investor may be able to continue with the case by notifying USCIS.

If the investor cannot continue under the original structure, the good-faith investor rules may provide two main options.

First, the NCE—the new commercial enterprise into which the investor invested—may be able to affiliate with another regional center. This can preserve the original investment structure if the project remains viable and the necessary parties are able to make the change.

Second, the investor may be able to make a further investment into another NCE. That further investment does not have to be the full $800,000. Under this relief path, the amount can be at least $500,000. If the original project did not create the required jobs, the investor may rely on jobs created through the new investment.

This option can matter for investors whose projects or regional centers run into trouble before the immigration process is complete. It can also help preserve the investor’s priority date and avoid forcing the investor to restart the EB-5 process from the beginning.

Recent regional center terminations have made this issue more pressing. Around March 2026, many investors were dealing with a 180-day deadline tied to earlier regional center terminations. The terminations had occurred about 180 days before that point, and investors had to act within that window. Many used the regional center termination provision to try to preserve their EB-5 cases.

Debarment Remains Unclear

Debarment is the other major good-faith investor issue. In theory, debarment should help investors when a project has gone bad. In practice, the rules remain unclear.

USCIS has not clearly defined what debarment means. It has not issued clear standards for when a project should be debarred. It has not provided clear procedures for how investors can request or use debarment relief.

If a project is fraudulent or fails because of misconduct, investors may need USCIS to debar the project before they can use the full good-faith investor protections. But if USCIS does not debar the project, the investor may be blocked from using the relief Congress intended.

This issue can arise even in severe cases. A project may be clearly fraudulent. The SEC may have become involved. Investor funds may have been stolen. Even then, if USCIS does not formally debar the project, investors may still struggle to access debarment-based relief.

Debarment could be more useful than regional center termination in some cases. Regional center termination relief may require a further investment of at least $500,000. Debarment relief may allow an investor to invest less than $500,000, as long as the new investment creates the required 10 jobs.

That difference matters. An investor who has already lost most or all of the original capital may not be able to make another large investment. A lower reinvestment amount could make relief possible for families who otherwise would have no practical path forward.

For now, debarment remains one of the least settled areas of post-RIA EB-5 law. Litigation is already moving forward, and more disputes are likely. Until USCIS issues clearer guidance, investors in failed or fraudulent projects may face uncertainty even when they acted in good faith.

Reinvestment May Help Some Investors Preserve Their EB-5 Cases

Some investors facing regional center termination or project failure may be able to reinvest all or part of their original capital commitment into a new NCE. This can allow the investor to keep moving toward EB-5 approval instead of losing the case entirely.

This kind of solution must be structured carefully. The new investment must fit within the applicable good-faith investor rules. It also must create enough jobs to support the investor’s immigration case. The investor’s attorney should review the facts, the USCIS notices, the timing, and the available project options before any reinvestment decision is made.

EB5AN has structured three offerings for investors in this type of rescue-investor situation, including Spring Haven. At least one I-526E approval has already been received in one of those offerings.

I-829 Denial Risks: Job Creation, Sustainment, Redeployment, and Immigration Court

I-526E approval does not end the EB-5 process. Even after an investor receives a conditional Green Card, the case is still only partway complete. The investor must later file Form I-829 to remove conditions and become a lawful permanent resident without conditions.

The I-829 petition is filed after the investor has held conditional permanent residence for 21 months. At that stage, USCIS reviews whether the investor satisfied the core EB-5 requirements. The main questions are whether the required jobs were created and whether the investment was sustained.

These issues are now receiving closer review. USCIS is asking more questions about job creation, project spending, sustainment, redeployment, and even source of funds that USCIS already approved at the I-526E stage.

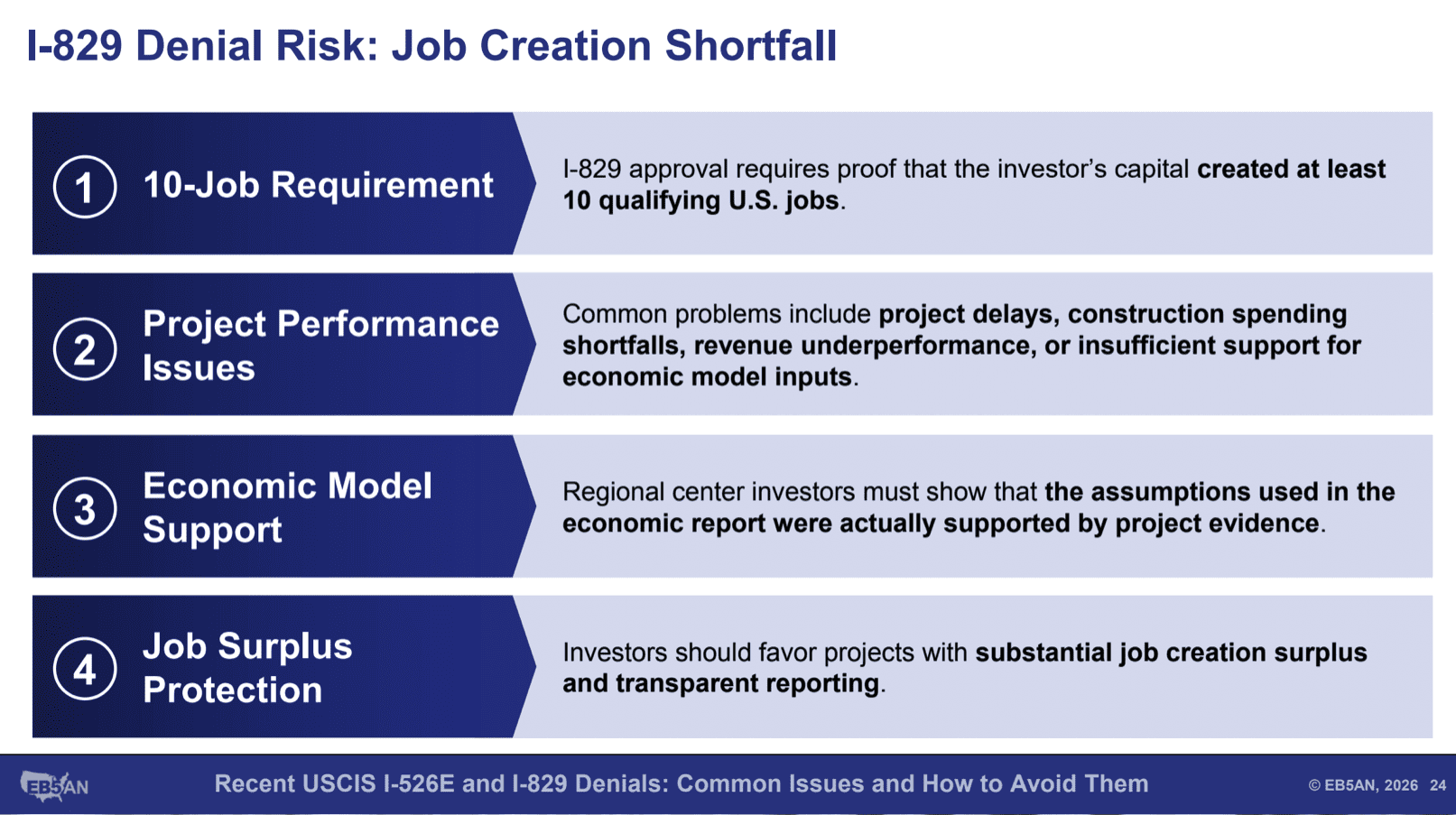

Job Creation Is the Central I-829 Issue

The main purpose of the I-829 petition is to show that the EB-5 investment created the required jobs. In most cases, each EB-5 investor must be credited with at least 10 qualifying jobs.

The job-creation analysis depends on the type of EB-5 investment. Regional center cases and direct EB-5 cases raise different problems.

In a regional center case, the issue may be a job shortfall. For example, if a project created 100 jobs but has 15 investors, the project needs 150 jobs to support every investor. That creates job-allocation questions. USCIS may examine which investors receive credit first and whether the documents support that allocation.

A regional center filing may also need to show that more jobs were created than originally expected. At the I-526E stage, the project may rely on projections. At the I-829 stage, USCIS wants to know what actually happened.

That means USCIS may examine the project’s actual hard construction costs, soft costs, furniture, fixtures, equipment expenses, and timeline. Those facts can affect the economic analysis that supports job creation.

Direct EB-5 cases raise different issues because the investor is often counting actual employees. The evidence may need to show that each employee worked at least 35 hours per week. It may need to show that the employees were W-2 employees, not 1099 contractors It may also need to show that the employees were U.S. citizens or permanent residents and that the positions were permanent.

A common problem arises when a business created the jobs but later reduced staff. For example, a business may have had 12 qualifying employees and later dropped to seven. The legal argument is that the investor must prove the jobs were created, not that every job still exists at the time of adjudication. But USCIS may still raise this issue in RFEs and NOIDs.

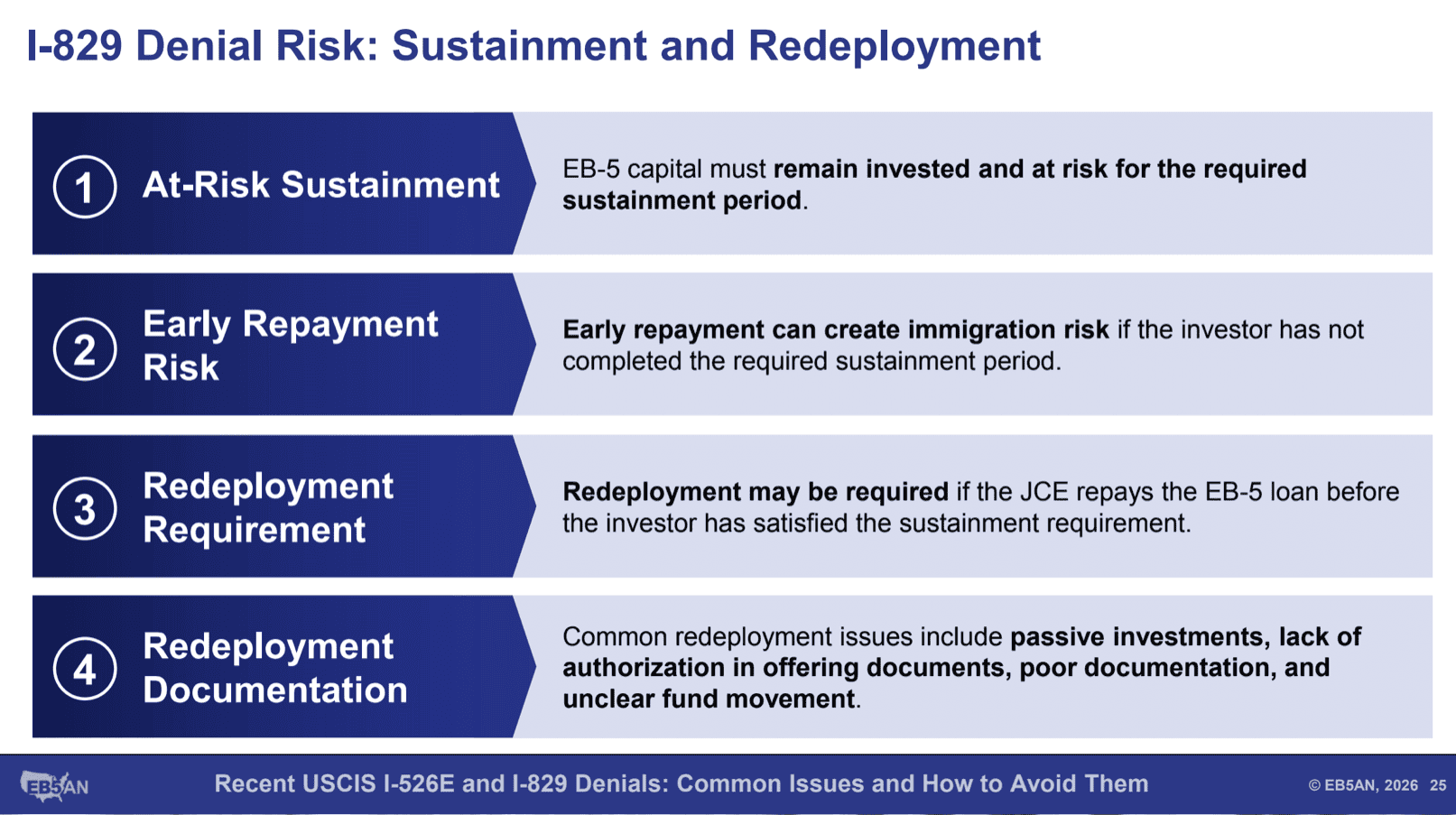

Sustainment Is Becoming a More Complicated Issue

Sustainment is another major I-829 issue. In general, the investor must show that the EB-5 capital remained invested for the required period. But USCIS appears to be asking more questions about what sustainment means and how it should be proved. The sustainment analysis can differ for pre-RIA and post-RIA investors. Pre-RIA investors generally must sustain the investment during the two-year conditional residence period, while post-RIA investors are subject to the RIA’s separate two-year investment timeframe, subject to USCIS guidance and job-creation requirements.

Investors should keep in mind what sustainment really means in the EB-5 program. If an investor places $800,000 into the NCE and has not received that money back, the investor has generally sustained the investment. A separate issue is whether the NCE made the money available to the JCE and whether the JCE used the funds for job creation.

USCIS can sometimes blur these concepts. The question of whether the funds were made available to the JCE relates to a separate EB-5 requirement. It should not be confused with whether the investor sustained the investment.

Still, the strongest I-829 record should show both points clearly. It should show that the investment was not returned to the investor. It should also show that the funds were used by the JCE to build the project, operate the business, or otherwise support the claimed job creation.

Redeployment Is Receiving New Attention

Redeployment is also becoming a more active area of USCIS review at the I-829 stage.

For a long time, USCIS asked few questions about the details of redeployment. That is changing. USCIS is now asking where redeployed funds went and whether the redeployment target was an active business.

This can matter when the original project has already repaid the NCE before the investor’s sustainment period is complete. In that situation, the capital may need to be redeployed into another qualifying activity. USCIS may then ask whether that redeployment was proper and whether the funds remained at risk.

Investors should expect more questions in this area. The I-829 filing should be ready to explain the flow of funds, the reason for redeployment, where the money went, and how the redeployed capital continued to satisfy EB-5 requirements.

Faster I-526E Adjudications Can Create Timing Problems

Recent faster I-526E adjudications have created another practical issue.

Some investors assume that EB-5 funds must remain at the JCE level for two full years before the I-829 petition is filed. Many regional centers use conservative standards and try to make sure funds reach the JCE level and stay there for a full two years.

But faster I-526E processing can make that difficult. USCIS has adjudicated many I-526E petitions quickly under the RIA. If an investor receives a fast approval and becomes a conditional permanent resident sooner than expected, the I-829 filing deadline may arrive before the project has had a full two years to absorb and use the capital at the JCE level.

That does not necessarily mean the investor has failed to satisfy EB-5 requirements. But it does mean the I-829 filing may need to explain the timing carefully. The record should show when the funds were invested, when they were made available, how they were used, and why the project timeline supports approval.

USCIS Is Reexamining Source of Funds at the I-829 Stage

One of the most troubling recent trends is USCIS readjudicating source of funds at the I-829 stage.

In these cases, USCIS may have already approved the investor’s I-526E petition and source-of-funds documentation. The investor may have then immigrated to the United States, sold a business overseas, sold a home, moved children into U.S. schools, and built life around the approval. Years later, USCIS may revisit the same source-of-funds record and deny the I-829 based on standards it applies later.

The investor may have done nothing wrong. The investor may not have hidden anything or made false statements. But USCIS may still decide that it no longer accepts the source-of-funds record that supported the original approval.

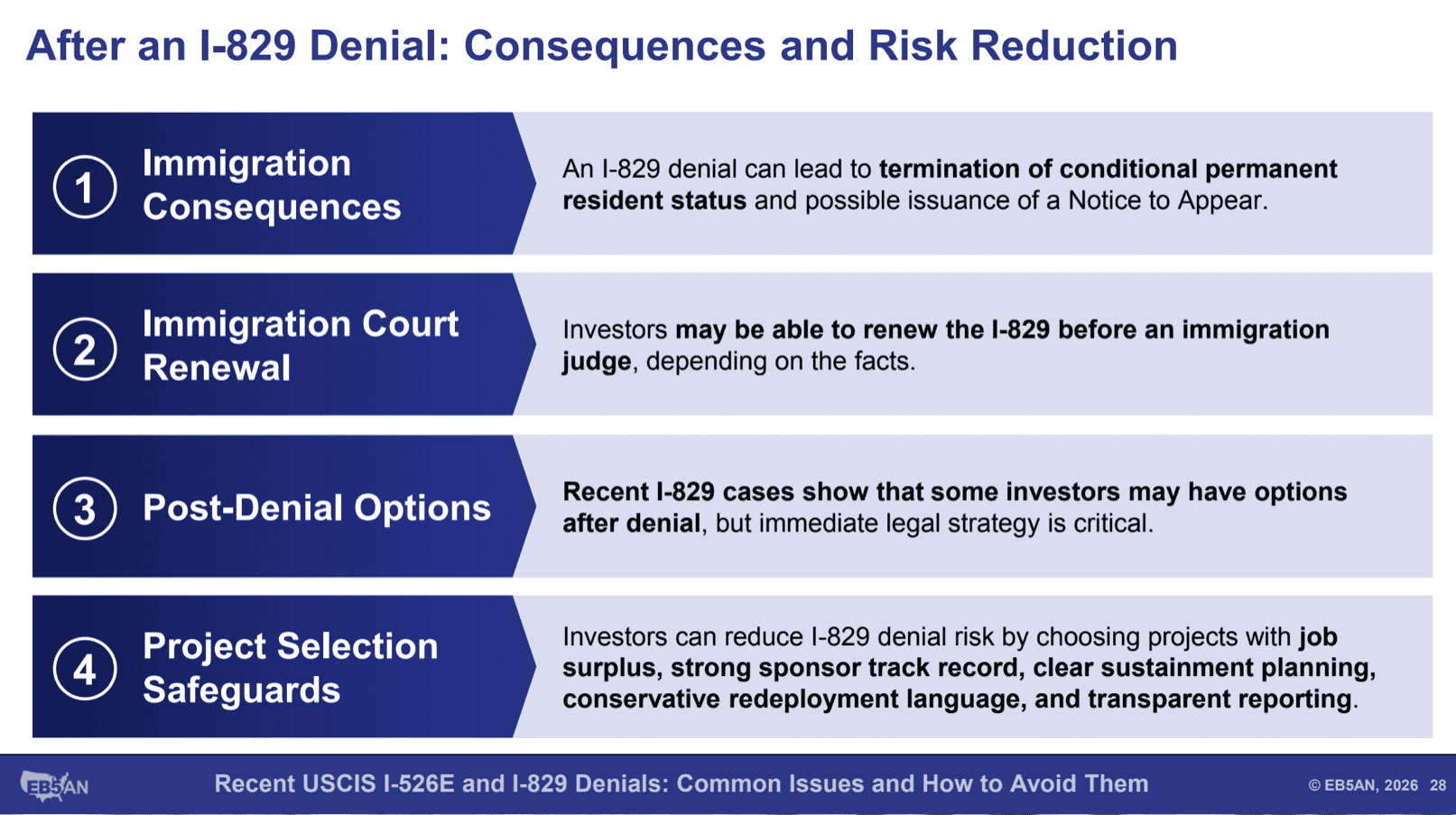

Current I-829 denials are being issued for several reasons. Some are based on source of funds. Others are based on sustainment or job creation. When USCIS denies an I-829, the process becomes very different from an I-526E denial.

An I-526E denial can be challenged in federal court, but an I-829 denial cannot go directly to federal court. It must go before an immigration court.

Immigration Court Creates Delay and Uncertainty

The immigration court process can take years. Federal court litigation over an I-526E denial may lead to a decision in about a year. I-829 cases in immigration court can take much longer. Some are scheduled for 2028 and 2029. Others may be scheduled sooner, in 2026 or 2027, but long delays remain a real possibility.

There is one meaningful advantage for investors in immigration court. In an I-526E filing, the investor has the burden of proof. In immigration court after an I-829 denial, the government has the burden. If USCIS claims that the investor’s funds were not lawful, the government must prove that point.

In many cases, the government may not be prepared to present witnesses or evidence showing that the funds were unlawful. For that reason, some I-829 denial cases can be won before an immigration judge, even without extensive new evidence.

Still, the process can be long and disruptive. Investors often have families, homes, jobs, and children in school in the United States by the time an I-829 denial occurs. A denial can place the family in a difficult position with limited choices.

What Happens After an I-829 Denial

An I-829 denial does not usually mean the investor must immediately leave the United States. After an I-829 denial, the investor should immediately consult immigration counsel regarding status, work authorization, travel, I-551 documentation, and review in removal proceedings. They should be able to continue receiving I-551 stamps. They should also be able to keep working and studying in the United States.

The biggest practical problem is travel. Investors in this position may be unable to leave the United States for a long period of time. That can affect family obligations, business responsibilities, and personal plans outside the country.

For many investors, the only real option is to appeal the denial. By the I-829 stage, the family may already be deeply settled in the United States. The stakes are high, and the process can be slow. But some cases are winnable, especially where USCIS is trying to revisit source of funds without enough evidence to meet its burden in immigration court.

The I-829 stage should therefore be treated with the same care as the I-526E stage. Investors should preserve records, track job creation, understand sustainment, document redeployment, and work with experienced EB-5 counsel before problems arise. A conditional Green Card is a major step, but it is not the end of the EB-5 process.

EB-5 Investors Should Prepare Before USCIS Raises Questions

The recent increase in USCIS scrutiny should change how investors approach EB-5. A strong project is still essential, but it is not enough by itself. Investors also need clean source-of-funds documentation, a clear immigration history, careful loan or partial-funding structures, and a plan for the I-829 stage from the beginning.

Investors who are facing a regional center termination, project failure, RFE, NOID, or denial should act quickly. The RIA created relief options for good-faith investors, but those options are technical and time-sensitive. Waiting can reduce the investor’s ability to preserve the case.

The best protection is to prepare now and retain an experienced immigration attorney. EB-5 remains one of the strongest paths to U.S. permanent residence for many families, but the process now requires more care at every stage. Investors should work with a skilled EB-5 immigration counsel, choose projects with strong documentation, and review the full record before filing.

With the right guidance and a well-documented filing, investors can reduce avoidable risk and move through the EB-5 process with greater confidence. We invite you to schedule a free consultation with EB5AN to explore your immigration options and secure your U.S. Green Cards.